Table of Content

The lender must be in receipt of the counseling certificate before they will close the mortgage. To locate a reverse mortgage counselor close to you, contact your loan originator or your local HUD workplace. The fees and cost of a reverse mortgage are based on a quantity of items.

You at the moment are leaving AARP.org and going to a website that's not operated by AARP. A different privacy policy and phrases of service will apply. Discover extra resources onfinanceandtaxeson the NU Resource Center. In basic, the older you are, the extra equity you have in your house, and the much less you owe on it, the more money you may get. The FTC and its legislation enforcement partners introduced actions in opposition to a quantity of income scams that conned individuals out of lots of of hundreds of thousands of dollars by falsely telling them they may make a lot of money.

Can My Heirs Contact A Hud-approved Counselor Or My Mortgage Servicer On My Behalf?

The Arntzes, who stay footsteps from the Intracoastal Waterway, cannot think about transferring. GreenPath consultants might help seniors think through options like growing a strong finances or pursuing a debt management plan. It's a financial product that allows you to entry the equity in your house and convert it into tax-free money.

You make a change within the existing HECM by telling your servicer what you want to do, and paying $20 for the trouble. To refinance, of course, you should re-enter the market, ideally to acquire a new kosher HECM. Borrowers with an unused credit score line can convert it to a monthly fee. You are there, simply click on on Rates and Fees on the top of this web page to see the costs on both fastened and adjustable-rate HECMs reported by 9 lenders each week. It also shows weekly historical figures beginning August 2, 2016.

What Are The Other Ways I Can Obtain My Proceeds?

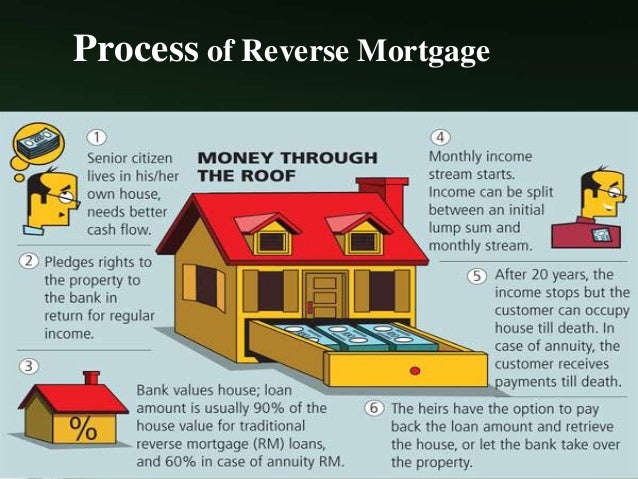

Moreover, said applicant should have the power to claim the home as his or her main place of residence. Lastly, all prospective debtors should present evidence indicating the possession of enough monetary sources to cover continued upkeep, insurance, and taxation charges. A reverse mortgage is an option out there to owners age 62 and older to borrow in opposition to their home’s equity without having to make monthly mortgage payments.

There isn't any express requirement, however your equity have to be giant sufficient to cowl the present mortgage balance. If your house is worth $200,000 for example, your loan balance needs to be lower than $100,000. How a lot much less varies with age and with the worth of the HECM. Struggling with paying property-related bills, contact your reverse mortgage servicer for assistance. As lengthy as you reside in the house as your major residence, maintain the house, and pay property-related bills on time, the loan does not need to be repaid.

Rejecting A Reverse Mortgage

You wish to enhance your current and future month-to-month earnings as a lot as attainable. Your servicing agent will use any remaining unused borrowing energy in your HECM to pay the costs. If you have not any borrowing power left, the servicing agent will request permission from FHA to provoke foreclosures proceedings. The threat is nowhere close to as nice as with a normal mortgage.

HECM reverse mortgages are unique in using two interest rates in each transaction. One rate of interest is used in calculating the borrower’s future debt and future credit score line if there's one. This is the “mortgage rate” and it is comparable to the speed on commonplace mortgages. Ignorance of HECM reverse mortgages is widespread as a end result of HECMs are sophisticated and really unlike the standard mortgages with which most seniors bought their properties.

No, you have to occupy the home as your main residence to qualify for a HECM reverse mortgage. In addition, the rule doesn't apply if the HECM is used to buy a home. If you purchase your HECM via my web site where you'll find a way to select the lender providing the most effective deal, it won’t matter whether the steadiness is paid off as a half of the HECM transaction, or paid by you beforehand. The second worst mistake, if they overcome the primary, is to put themselves within the arms of the lender whose commercial captured their eye. This may find yourself in their being over-charged on the rate of interest, the origination charge or each.

Just make sure you do the mathematics and realize the implications that a reverse mortgage may have upon any inheritance your children might be anticipating. Continue to fulfill obligations corresponding to property taxes, home-owner's insurance coverage, association dues, and repairs. While a reverse mortgage could be right for you, there could also be other choices. The reversal comes into play when contemplating that as funds are made on a conventional mortgage, the quantity owed lowered and the equity in the property increases over time. Yes, however whether it would be advantageous is dependent upon how rather more you presumably can draw relative to the incremental settlement prices of the new HECM. A rule of thumb is that the rise within the amount you can draw ought to be more than 5 times as massive as the settlement prices.

In order to qualify for a reverse mortgage, the Federal Housing Administration has mandated a quantity of necessities. First and foremost, any potential borrower should sixty two or older. Furthermore, an applicant should personal his or her house outright, or else have a minimally low excellent mortgage balance.

No, the loss is borne by the insurance reserve fund, into which all HECM borrowers contribute. If the borrower dies and the mortgage balance exceeds the property value, FHA assumes the loss. If the heirs want the house, they will purchase it for 95% of appraised value much less closing prices and Realtor fee. A credit score evaluation was not considered necessary as a outcome of HECMs haven't any required month-to-month fee. However, when tax delinquencies began to rise, HUD issued new laws to take care of it. Lenders are actually required to evaluate the capacity and willingness of applicants to fulfill their obligations.

A reverse mortgage is a home equity loan exclusively designed for individuals 62 or older. These cash funds, plus the lifetime elimination of any month-to-month mortgage funds, can immediately improve your monthly money circulate while additionally helping you meet your longer-term retirement goals. A reverse mortgage requires that you just keep your property and regularly pay your property taxes and owners insurance.

No comments:

Post a Comment